Trakm8 partners with CA Cars for driving instructor telematics

Trakm8 has confirmed a new 3 year partnership with Commercial Associates LTD, trading as CA Cars, to enhance the monitoring of vehicle health and tracking of vehicle mileage for the latter’s extensive fleet of dual-controlled vehicles supplied to driving instructors and their schools across the UK. Established in 1986, CA Cars is a family-owned business […]

Confidence and calm urged as used car values drop

Fleets and dealers should trust the data and maintain a cool head during a period of volatile values in the UK’s used car market, according to analysis from Cox Automotive. Cox Automotive’s confidence in its forecast persists as we approach the final weeks of 2023. Its year-to-date baseline forecast of 5,545,530 is within 99.7% – […]

SMMT data indicates 10th consecutive month of UK new car sales growth

The UK new car market has posted its longest uninterrupted period of expansion for eight years, as registrations grew 16.7% in May to reach 145,204 units according to the latest figures from the Society of Motor Manufacturers and Traders (SMMT). The performance marks 10 consecutive months of growth, although registrations remain -21.0% below pre-pandemic 2019 […]

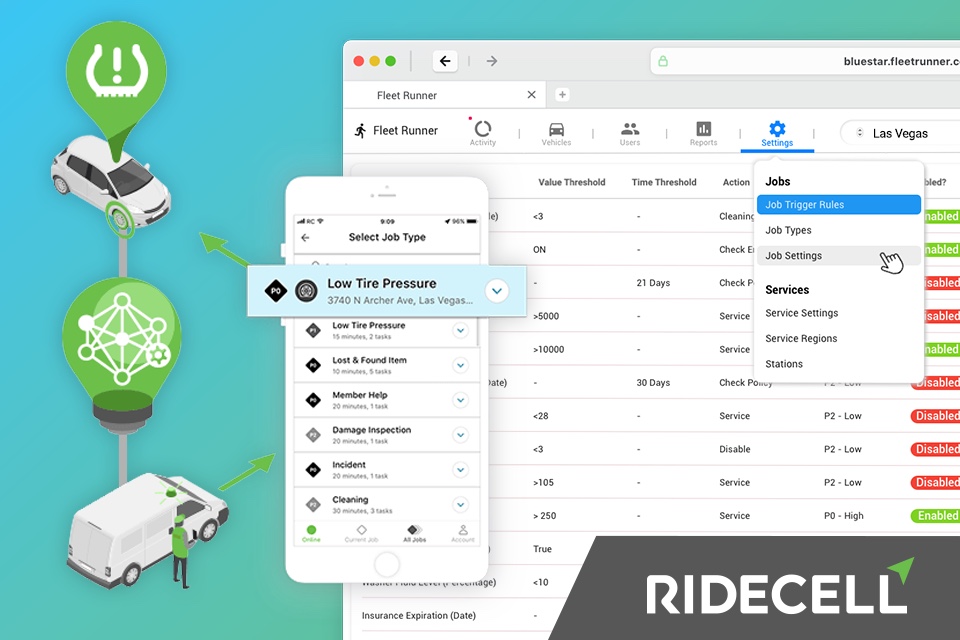

Turning fleet data insights into automatic actions

By Mark Thomas, EVP Marketing & Alliances, Ridecell How Automation Technology Can Transform Your Fleet Data has become invaluable for fleet-based businesses. Organizations are increasingly leveraging more data from telematics and dashcams, where everything from real-time engine diagnostics to crash detection is readily available. But while GPS tracking information and data dashboards provide benefits for […]

SMMT: UK car production down a fifth in 1H22 though shortages ease

UK car production declined -19.2% in the first six months of the year, according to figures published today by the Society of Motor Manufacturers and Traders (SMMT), with 95,792 fewer vehicles built compared with the same period in 2021. 403,131 units were built, representing the weakest first half since the pandemic-ravaged 2020 and worse than […]

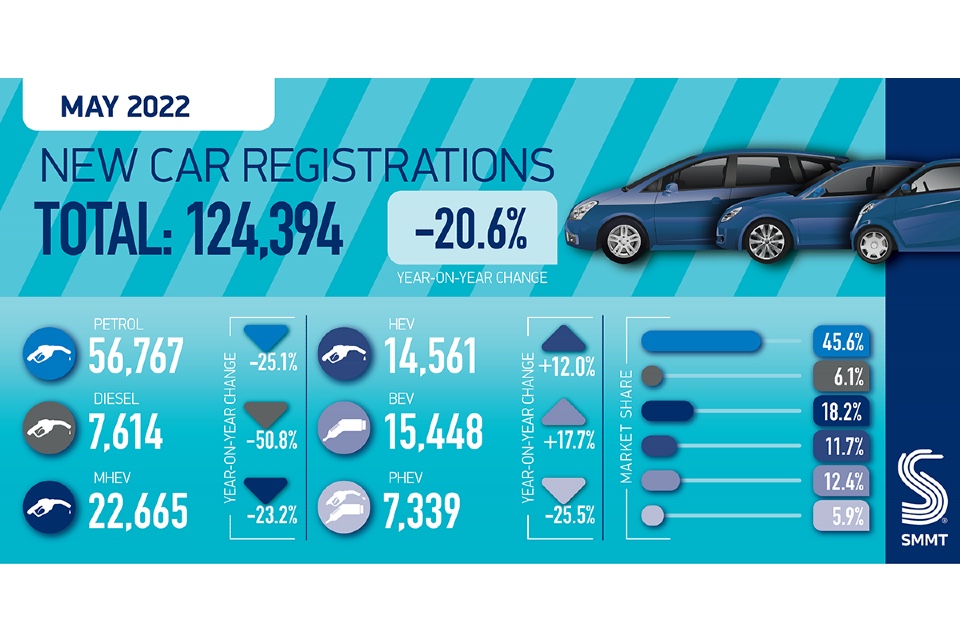

Supply chain issues see new car sales slump in May

New UK car registrations fell -20.6% to 124,394 units in the second weakest May since 1992, after the 2020 pandemic-hit market, as supply shortages continued to hamper new purchases and the fulfilment of existing orders, according to the latest figures from the Society of Motor Manufacturers and Traders (SMMT). The decline, compared with the first […]

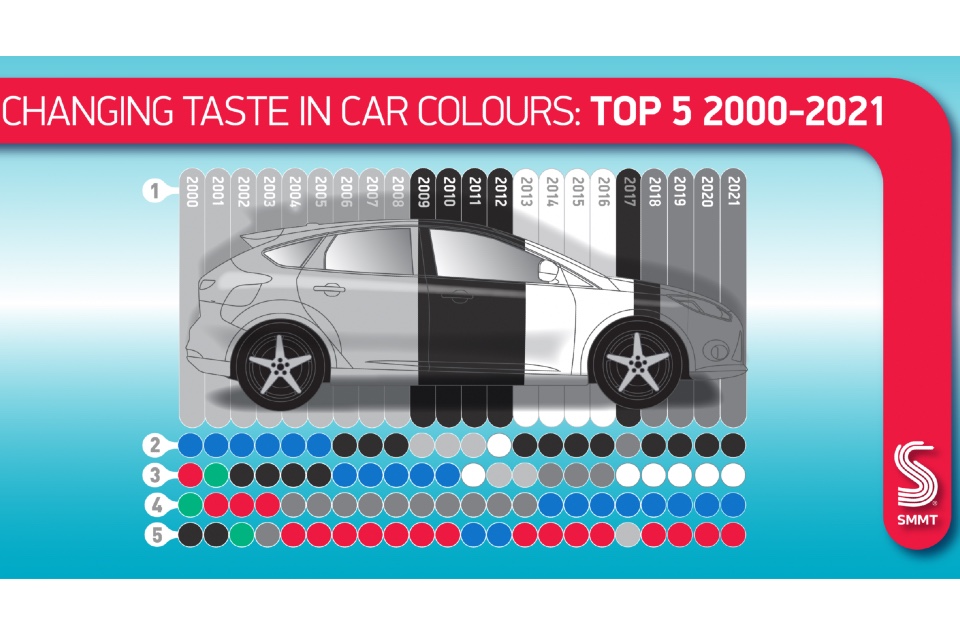

Grey is the colour… again!

British drivers doubled down on their preference for monochrome cars in 2021, with grey increasing its dominance as the UK’s favourite new car colour for the fourth year in a row, according to figures published today by the Society of Motor Manufacturers and Traders (SMMT). During a year of pandemic-related disruptions impacting total new car […]

The WhichEV View: JATO market data confirms massive increase in EV registrations in Europe

By James Morris, Editor, WhichEV For more than 30 years, Jato Dynamics has provided precision data on changes within the car market and their reports always make for interesting reading. Its latest update includes a summary of new vehicle registrations from across Europe for June 2021. With the pandemic seemingly well behind us now, the patterns are […]

Addressing privacy concerns in driver risk management

By Ed Dubens (pictured), CEO/Founder of eDriving Today, data security and privacy compliance are among the most important considerations for practically every business. For that reason, when reviewing digital driver risk management solutions, data security and privacy compliance are critical components of the assessment and planning phase, and can even be the deciding factor in whether a programme is […]

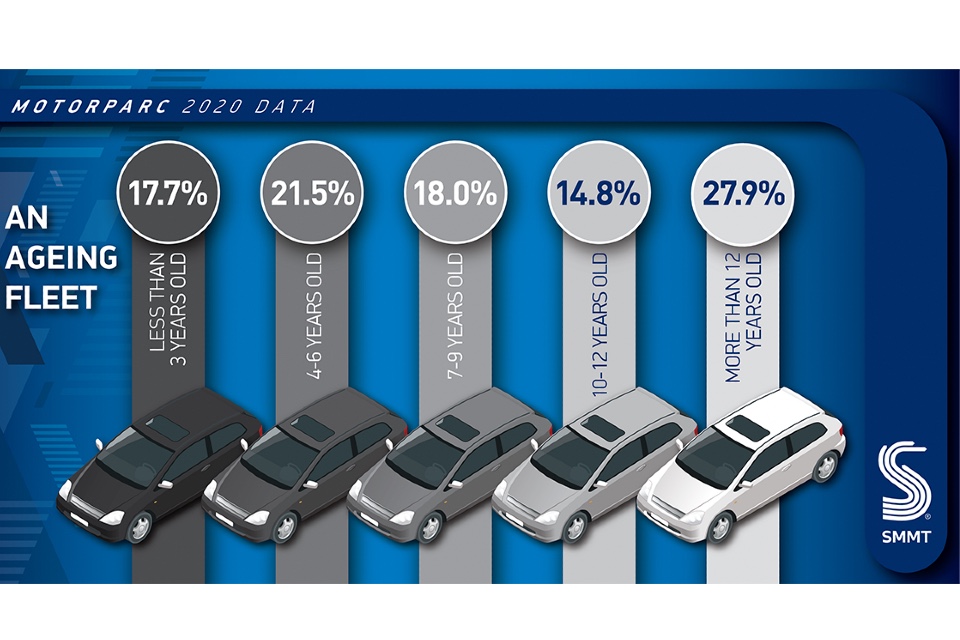

Motorparc: Total vehicles on UK roads falls to 40.35m

Vehicle numbers on UK roads fell to 40,350,714 in 2020, according to Motorparc data released today by the Society of Motor Manufacturers and Traders (SMMT), the first time the total number has fallen since the global financial crisis of 2009. As the pandemic stifled new vehicle uptake, the average age of cars on UK roads […]