UK EV population hits new high, says SMMT

The number of vehicles on British roads reached its highest ever level in 2024, rising by 1.4% to 41,964,268, according to new Motorparc data published today by the Society of Motor Manufacturers and Traders (SMMT). The number of cars in use also reached a new high, growing by 1.3% or 470,556 units to 36,165,401, marking […]

THE WHICHEV VIEW: The UK’s 2024 EV sales show the potential and challenges in the sector

By WhichEV In a year marked by both triumph and challenge, the UK’s automotive industry has achieved a significant milestone with record sales of electric vehicles (EVs) in 2024, despite not meeting the government’s ambitious Zero Emission Vehicle (ZEV) targets. As the nation progresses towards a greener future, the dynamics of the car market continue […]

Commercial van market returned to growth in August

The UK’s new light commercial vehicle (LCV) market returned to growth in August, rising 1.7% to record the best performance for the month since 2021 after two months of decline. According to the latest figures from the Society of Motor Manufacturers and Traders (SMMT), 16,575 vans, 4x4s, pickups and taxis joined the road in what […]

SMMT calls for new incentive plan to grow UK’s zero emission truck fleet

The UK Government should reform its ‘dated’ Plug-in Truck Grant to reflect the progress made by the sector in developing new zero emission truck technology and help cut CO2 by 18.8 million tonnes a year, according to calls from the Society of Motor Manufacturers and Traders (SMMT). The SMMT cites ONS data that shows that […]

THE WHICHEV VIEW: UK car market sees notable growth according to the SMMT

By WhichEV The UK’s new car market recorded a significant upturn, marking its 20th consecutive month of growth, with new car registrations climbing by 10.4%. This surge resulted in 317,786 new cars being registered, all sporting the new ’24’ numberplate, indicating the strongest March since 2019. However, this achievement still trails behind the pre-pandemic figures […]

SMMT data indicates 10th consecutive month of UK new car sales growth

The UK new car market has posted its longest uninterrupted period of expansion for eight years, as registrations grew 16.7% in May to reach 145,204 units according to the latest figures from the Society of Motor Manufacturers and Traders (SMMT). The performance marks 10 consecutive months of growth, although registrations remain -21.0% below pre-pandemic 2019 […]

Used EV sales up, but overall demand for second-hand cars falls

The UK’s used car market declined in 2022, down -8.5% to 6,890,777 transactions, according to the latest figures published by the Society of Motor Manufacturers and Traders (SMMT). The performance saw 640,179 fewer vehicles changing hands than in 2021, and remains -13.2% off 2019’s pre-pandemic total, as the squeeze on new car supply – primarily […]

SMMT: UK car production down a fifth in 1H22 though shortages ease

UK car production declined -19.2% in the first six months of the year, according to figures published today by the Society of Motor Manufacturers and Traders (SMMT), with 95,792 fewer vehicles built compared with the same period in 2021. 403,131 units were built, representing the weakest first half since the pandemic-ravaged 2020 and worse than […]

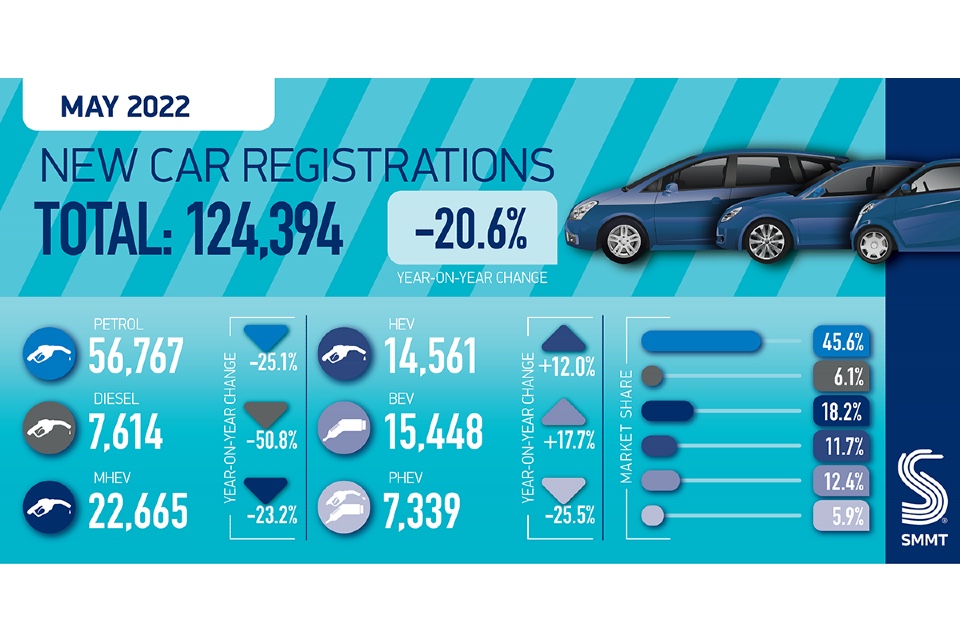

Supply chain issues see new car sales slump in May

New UK car registrations fell -20.6% to 124,394 units in the second weakest May since 1992, after the 2020 pandemic-hit market, as supply shortages continued to hamper new purchases and the fulfilment of existing orders, according to the latest figures from the Society of Motor Manufacturers and Traders (SMMT). The decline, compared with the first […]

SMMT calls for binding targets for chargepoint rollout as demand for EVs surges

The Society of Motor Manufacturers and Traders (SMMT) has published a seven-point plan calling for binding targets regarding the rollout of charging infrastructure across the UK. This nationally coordinated plan has been put forward to ensure every driver in Britain can benefit from an EV charging network that is affordable, available, and accessible Charging companies […]